Key points

– After the rough ride of 2021-22, 2022-23 turned out to be a good one for investors as shares rebounded thanks to falling inflation and hopes rates are near the top.

– Shares are at risk of a pull back as central banks remain hawkish and recession risks are high. However, returns over the next 12 months should still be reasonable as falling inflation takes pressure off central banks enabling rate cuts.

– The past financial year provides yet another reminder of just how hard it is to time investment markets – with shares rebounding just when everyone was most gloomy about inflation and interest rates. The key as always is to adopt a long term investment strategy and turn down the noise.

Introduction

The past financial year saw a solid rebound in investment returns, after the negative returns of the 2021-22 financial year. This note reviews the past 12 months in investment markets and looks at the outlook.

Inflation worries start to recede

Just as worries about inflation, recession and geopolitics drove poor returns in 2021-22, a relaxation of worries about these things drove a strong rebound in returns over the last financial year:

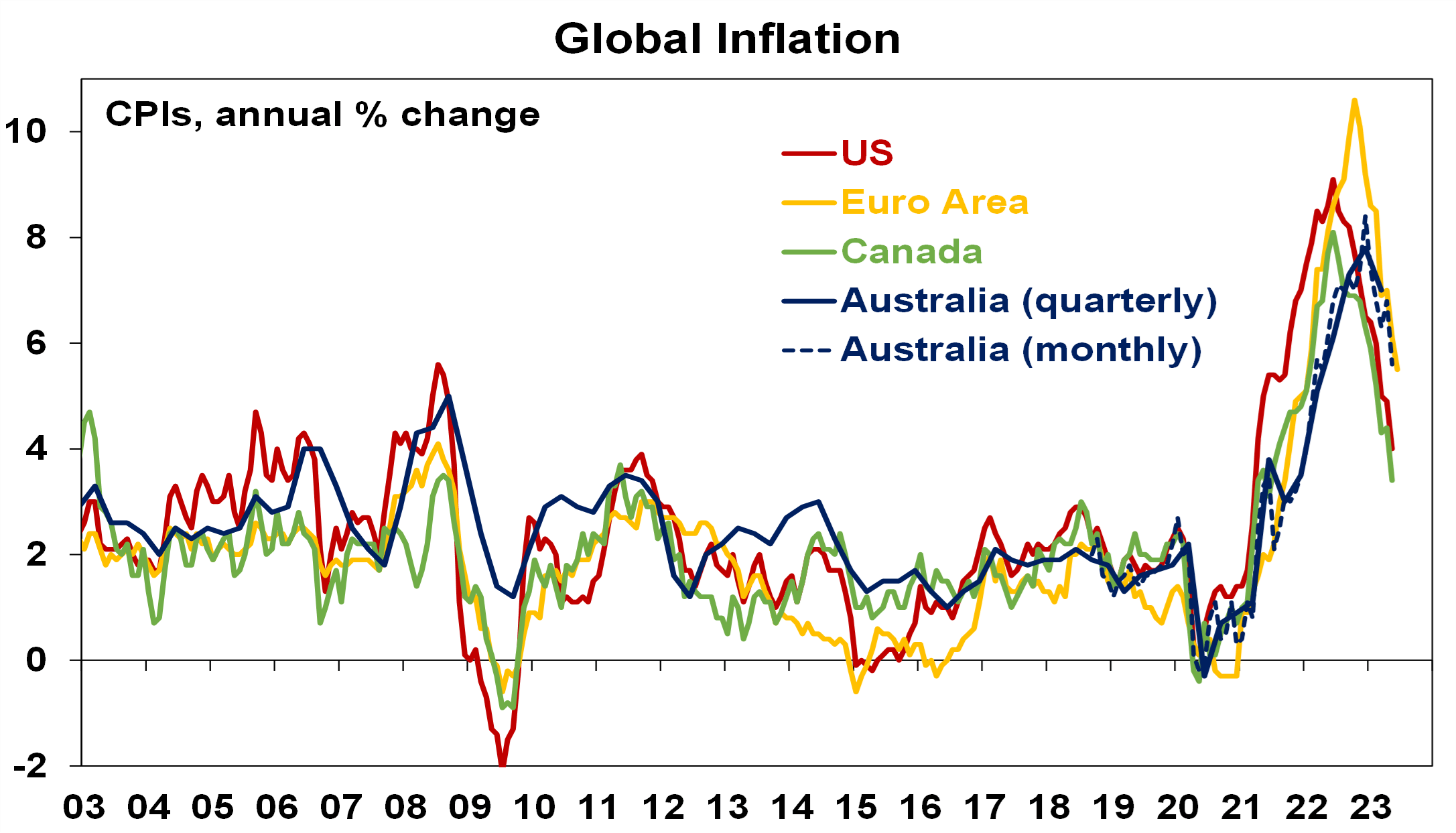

- While inflation rose to its highest in decades in 2022, it peaked in the US a year ago and has been trending down since with other countries following suit. Australia, which lagged on the way up, is doing the same on the way down. This reflects improved goods supply, lower commodity prices, lower transport costs and easing demand.

Source: Bloomberg, AMP

- While central banks still worry about sticky services inflation in the face of stronger wages growth, signs of cooling economic growth and slowing job openings have started to ease concerns on this front.

- This slowing in inflation has seen central banks slow the pace of rate hikes and provide confidence that they are near the top on rates.

- While the Eurozone entered a mild recession, global growth generally has held up better than feared with recession expectations getting pushed out. This in turn has supported profits.

- China reopened allowing its economy to bounce back – although so far, it’s been a bit weaker than expected in terms of manufacturing.

- Worst case fears regarding the war in Ukraine have not come to pass – with no escalation to NATO countries and Europe/Germany managing to move on from its reliance on Russian gas.

- Geopolitical tensions with China have got no worse with periodic talk of a thaw. This has occurred with China-Australian relations with the roll back by China of some restrictions on Australian exports.

- Enthusiasm for AI and its potential to boost productivity following the release of ChatGPT in late 2022 provided a boost for tech stocks.

Returns rebound

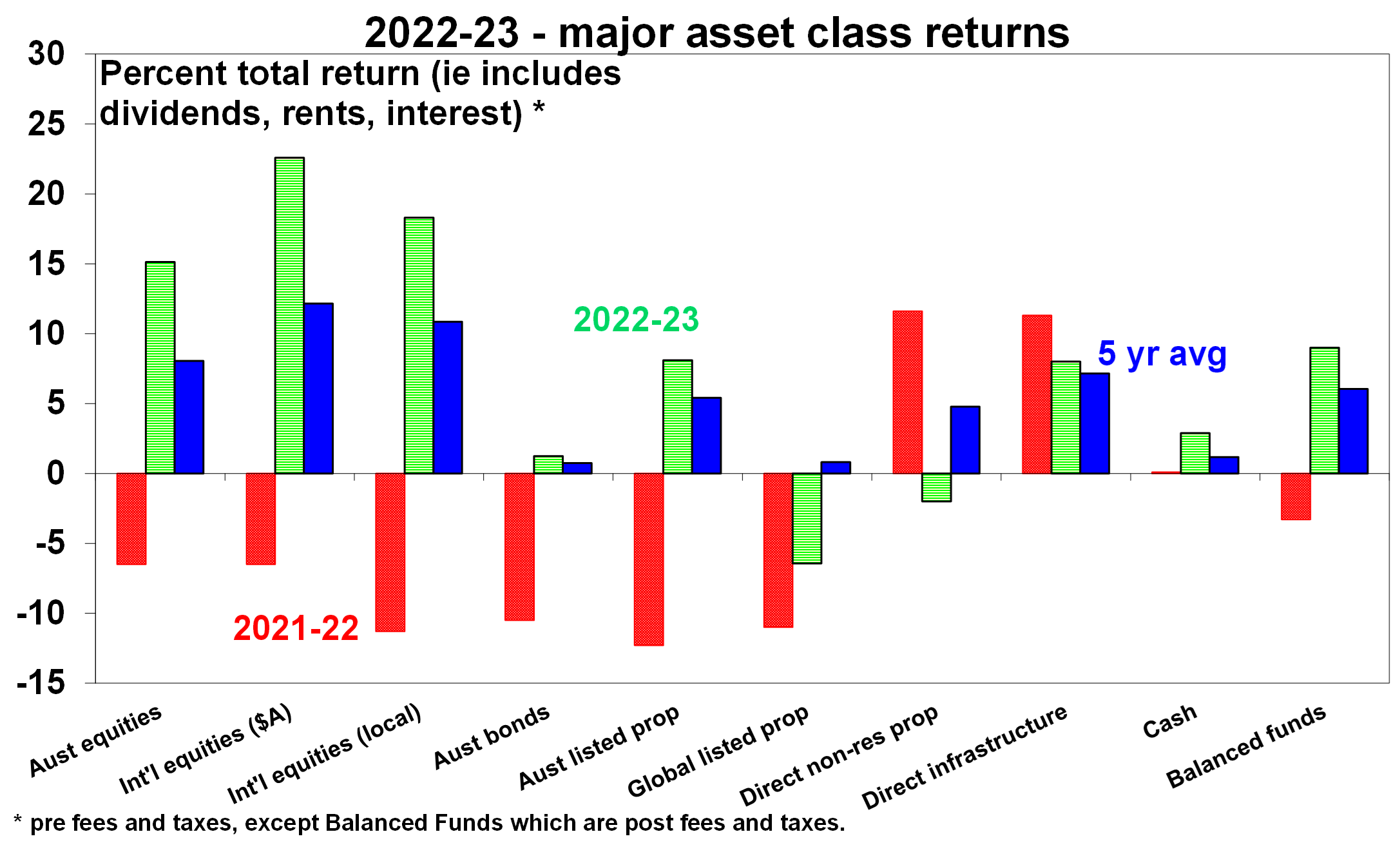

The net result has been a rebound in investment returns over the last financial year for most listed assets as can be seen in the next chart.

Source: Bloomberg, AMP

After seeing their worst loss in decades in 2021-22 as bond yields surged resulting in big capital losses, bond returns have stabilised over the last 12 months as bond yields stopped rising with higher yields helping.

Source: Bloomberg, RBA, AMP

Global shares returned 18% in local currency terms over 2022-23, with a fall in the $A (with lower commodity prices) boosting this to 23% in $A terms. Japanese and Eurozone shares outperformed, US shares benefitted from a rebound in tech stocks (helped by AI) and Chinese shares fell.

Australian shares returned 15%, benefitting from the positive global lead but were relative underperformers over the last six months as the RBA turned relatively more hawkish than had been expected driving worries about an Australian recession and with concerns about the strength of China’s recovery weighing on commodity prices and resources stocks.

Australian real estate investment trusts benefitted from better valuations and a stabilisation in bond yields but global REITs remained under pressure.

Unlisted commercial property returns look to have been negative as the lagged negative impact of higher bond yields and reduced space demand for office and retail property weighed on capital values.

Australian residential property prices fell 5.3%, reflecting a sharp fall in the second half of 2022 as higher mortgage rates hit but saw some recovery in the last 4 months as immigration rebounded and supply fell.

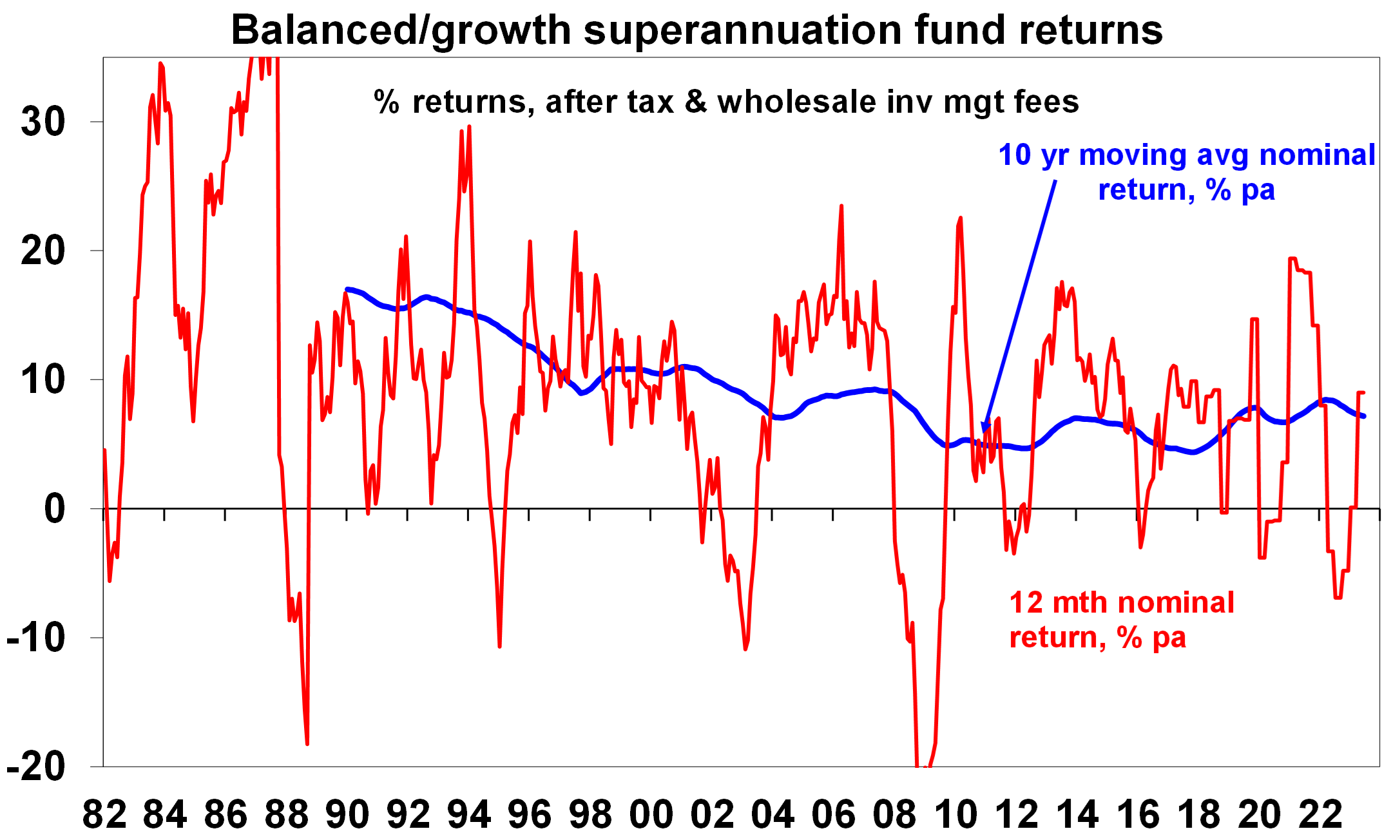

Combined, this drove an estimated 9% return in balanced growth superannuation funds. This is a big turnaround from the 3.5% or so loss from such funds in the previous financial year.

Source: AMP

The last few financial years has seen a bit of a zig zag pattern in returns with average super funds seeing losses in 2019-20 (as the pandemic hit), very strong returns in 2020-21 (as markets rebounded), a loss in 2021-22 (as inflation and bond yields surged) and now a rebound. Given the volatility it’s best to focus on their longer term average returns which have been 7.2% pa over the last decade or around 4.5% pa after inflation.

Some lessons from 2022-23

The big lesson of 2021-22 was that inflation was not dead, just resting and can raise its head to cause mayhem when the circumstances are right; but there were two big lessons over the last year. The first was that just as easy money was a major contributor to inflation in 2021-22 the move to tight money looks to be working to bring inflation back under control again albeit there is a way to go yet. The second was yet another reminder of just how hard it is to time markets. Just when everyone was most gloomy about inflation and interest rates, share markets rebounded.

Shares at risk of a correction

The bad news is that the risk of a near correction in shares is high. Shares had strong gains in June and are now overbought technically. Leading economic indicators continue to point to a high risk of recession in the US and the risk of recession in Australia is now around 50%. China’s recovery is looking less robust than expected and policy stimulus there so far has been pretty modest. Central banks are probably close to the top but they remain hawkish with a high risk of going too far. Risks also remain in relation to Ukraine – particularly with Putin looking to re-establish his authority after the Wagner mutiny in Russia. And while the month of July is often good for shares (particularly in Australian shares after June tax loss selling is reversed) the period to September-October is often rough.

Unlisted property returns are also likely to be negative over the year ahead as weak economic activity and the adjustment to working from home result in rising office property vacancy rates and more downwards pressure on property values.

The good news

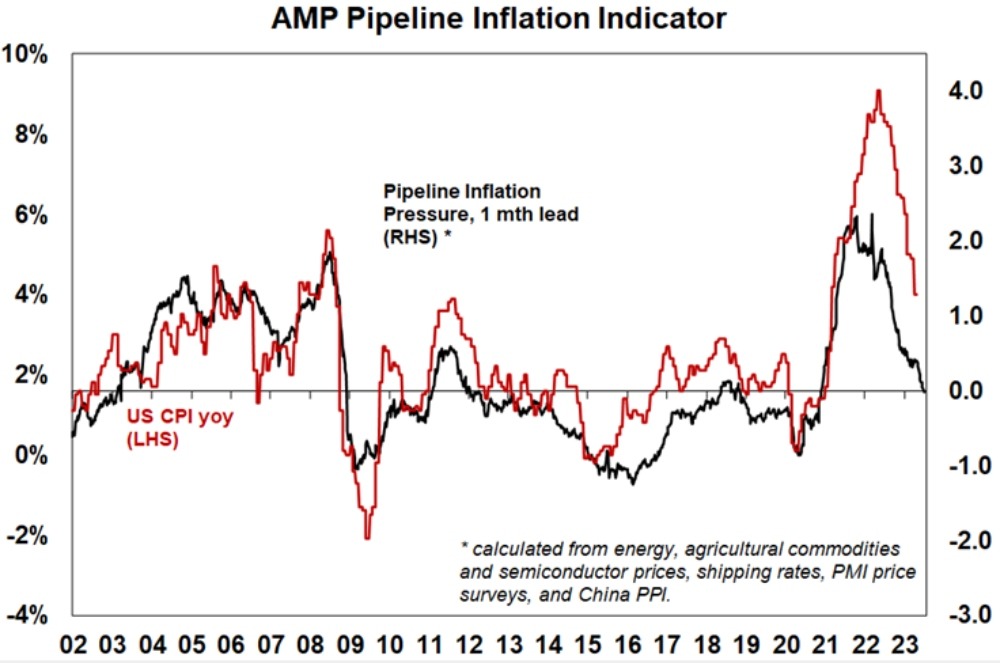

Fortunately, inflation rates are already falling without recession and our US Pipeline Inflation Indicator points to a further fall in inflation ahead.

The Inflation Pipeline Indicator is based on commodity prices, shipping rates and PMI price components. Source: Bloomberg, AMP

This should enable central banks to start easing monetary policy through next year in order to at least avoid a deep recession. In Australia, we expect the RBA’s cash rate to peak around 4.6% with four rate cuts through 2024. Moreover, global economic conditions have proven more resilient than investors feared, the rebound in US shares from their lows last year has broadened out to include more cyclical stocks (which is a positive sign) and investor positioning is still relatively cautious (which is arguably positive from a contrarian perspective).

So, while shares are vulnerable to a near term correction, returns over the next 12 months should still be reasonable albeit slower than they have been over the last 12 months. At the same time bond returns should be positive as bond yields settle down with falling inflation.

Overall balanced growth super returns are likely to be reasonable – but more like 6 to 7% than the 9% or so seen over the last financial year.

Things for investors to keep in mind

Of course, short term forecasting and market timing is fraught with difficulty and it’s best to stick to sound long term investment principles. Several things are always worth keeping in mind: periodic and often sharp setbacks in shares are normal; selling shares or switching to a more conservative superannuation strategy after falls just turns a paper loss into a real loss; when shares and other investments fall in value they are cheaper and offer higher long term return prospects; Australian shares still offer an attractive dividend yield versus bank deposits; shares and other assets invariably bottom when most investors are bearish; and during periods of uncertainty, when negative news reaches fever pitch, it makes sense to turn down the noise around investment markets in order to stick to an appropriate long term investment strategy.

Source: AMP